The Invention of Coinage

The Kingdom of Lydia creates the first standardized metal currency.

Stamped Metal and the Abstraction of Value

When the kings of Lydia first struck lumps of electrum—a natural gold-silver alloy panned from the Pactolus River near their capital at Sardis—sometime in the late seventh century BC, they did something stranger than mint money. They abstracted trust. A coin is a promise that a stamp can stand in for a thing, that authority can certify worth so two strangers need not weigh and bite the metal themselves. This was the monetization of confidence, and it would ripple forward through every market that followed.

The Deep Preconditions

Coinage was a late fruit of a very long tree. It presupposed agriculture (sv-agriculture) and the storable surpluses that made trade worth the trouble, and the dense, hierarchical cities that grew from those surpluses. It required metallurgy refined over millennia and, crucially, the prior invention of writing and reckoning—the accountancy that began with cuneiform (sv-cuneiform) on Mesopotamian clay and the codified, quantified justice of Hammurabi (sv-hammurabi), whose law already fixed prices and silver weights. Lydia sat at the seam between the Anatolian interior and the Greek-speaking Aegean, a crossroads thickened by trade in the centuries after the Late Bronze Age Collapse (sv-bronze-collapse) reshuffled the old palace economies. Earliest coins are usually placed in the reign of Alyattes (c. 630–585 BC); his successor Croesus, proverbial for wealth, is credited with the first reliably pure gold and silver issues and the world's first bimetallic standard.

How It Reshaped What Came After

The Greek cities seized the idea and ran. Coinage spread across the Aegean within a century, and it is no accident that the same Ionian world that produced standardized money also produced the first standardized thinking. Thales of Miletus (sv-thales) and the wider Pre-Socratic project (sv-presocratics) asked what single underlying substance all things were "made of"—a question that mirrors a coin's logic, where heterogeneous goods reduce to one common measure. Heraclitus (sv-heraclitus), an Ephesian from the Lydian sphere, wrote that all things are an exchange for fire as goods are for gold. Money and metaphysics were learning the same trick of abstraction in the same place at the same time.

Politically, coinage helped fund and define the polis. Coined wages and public payments underwrote the participatory machinery of Athenian democracy (sv-athenian-democracy), and Aristotle (sv-aristotle) would later theorize money as the universal mediator of exchange. Coinage also financed empire: it paid the armies of Alexander (sv-alexander), whose conquests flooded the Hellenistic world with portrait coinage as propaganda, a practice the Roman Republic (sv-roman-republic) and then Augustus (sv-augustus) perfected into the emperor's face in every purse.

The Long Thread Forward

The deeper invention was not the metal disc but the principle that value could be a sign rather than a substance. That principle survived the loss of precious metal entirely. The double-entry ledgers of the Italian Renaissance (sv-renaissance), the paper credit of the Industrial Revolution (sv-industrial-revolution), and eventually the purely informational money of the World Wide Web (sv-www) all extend the Lydian leap: trust, abstracted and made transferable. Even the contemporary turn toward biology and intelligence as information—Kurzweil's claim that biology becomes information technology (sv-kurzweil-genome)—rhymes with this ancient gesture. A coin was humanity's first proof that a stamp of authority could turn a physical thing into a portable, exchangeable symbol. Money was, in a sense, our earliest information technology, and from a riverbank in Anatolia it taught the species to trade in signs.

Global Context

Coinage emerged in western Anatolia just as the great Near Eastern political order was collapsing and reconfiguring. The Neo-Assyrian Empire, which had dominated the region for centuries, was disintegrating: Nabopolassar seized Babylon in 626 BCE, and a Medo-Babylonian coalition sacked Nineveh in 612 BCE. Lydia, under the Mermnad dynasty (Gyges to Alyattes to Croesus), filled part of the resulting power vacuum in Asia Minor, profiting from electrum dredged from the Pactolus near its capital Sardis. To the west, the Greek poleis were entering the Archaic crisis that would produce Solon's debt-cancelling reforms at Athens in 594 BCE. In the eastern Mediterranean, Saite Egypt under Psamtik I had reasserted independence using Greek and Carian mercenaries. Farther east, the Chinese states of the Spring and Autumn period contended within a weakening Zhou order, and northern India approached the urbanizing second-millennium-of-cities horizon. Coinage was thus born amid the same turbulent seventh-century world that classicists associate with the dawn of the "Axial Age."

The Paradigm Shift

Coinage fused three older technologies—weighed bullion, the sealing of property, and standardized metallurgy—into a radically new instrument: a portable, fungible, state-authenticated unit of value. Earlier Near Eastern economies had used silver by weight (shekels) for millennia, but each transaction required scales and trust in purity. The Lydian innovation was to stamp small electrum dumps with a punch and device, so that an issuer's mark guaranteed weight and acceptance, eliminating per-transaction assay. Within roughly a century the idea spread explosively across the Greek world, where Aegina, Athens, and Corinth struck silver, and it underwrote the monetized polis, mercenary armies, market exchange, and—Richard Seaford argues—even abstract philosophical concepts of impersonal universal value. Coinage shifted economic power toward issuing authorities and broadened participation in exchange beyond palace and temple. The trajectory ran straight from Croesus's bimetallic Croeseids through the Persian daric, Athenian "owls," and Roman denarius to every minted currency since, making the stamped coin one of antiquity's most consequential and enduring inventions.

Counterfactual: What If It Had Gone Differently

Had coinage not been invented in Anatolia around 630 BCE, monetized exchange would not necessarily have failed to emerge—but its form and timing would likely differ. Mesopotamia had operated sophisticated silver-by-weight economies for two millennia without coins, suggesting that complex commerce does not require coinage; David Schaps stresses precisely this point, noting that the Greeks' rapid, near-universal adoption was historically peculiar rather than inevitable. Without the Lydian model, the explosive Greek monetization of the sixth–fifth centuries that funded triremes, mercenaries, and democratic pay (misthos) might have been slower or weaker, plausibly altering the Persian Wars and the rise of Athenian power. Counterfactually, weighed-bullion or stamped-ingot systems (as in Achaemenid Persia's early adoption) could have predominated longer. Yet the convenience advantage was so decisive that some independent invention of struck money elsewhere—China's bronze cash arose separately—seems probable. The strongest claim is narrower: the specifically Greco-Lydian coin, and the cultural and conceptual revolution Seaford ties to it, were contingent on this particular regional moment.

Scholarly Debate

The central debate concerns why electrum coinage appeared and who initiated it—the state or private actors. Robert Wallace argued that Lydian/Ionian governments minted electrum to stabilize and standardize a notoriously variable alloy, imposing a fixed exchange value (and likely extracting profit, since coins' face value exceeded intrinsic gold content). David Schaps countered that the earliest electrum bears no numerals or value marks, complicating any straightforward "state guarantee" reading, and emphasized coinage's later transformative monetization of Greece. David Graeber and others proposed bottom-up origins, with jewellers or merchants striking guaranteed pieces before states monopolized issue. A further axis, advanced by Richard Seaford, treats coinage as cause and symptom of a cognitive shift toward abstract, impersonal value reflected in Presocratic philosophy. Chronology is itself contested: Koray Konuk, the Sardis numismatists (Kroll), and the Austrian Academy's project debate whether the Ephesian Artemision deposit dates coinage to the mid- versus third-quarter seventh century, and whether Lydia or Ionian Greek cities struck first.

How It Connects

What Made It Possible

- Mesopotamian economies had used silver as a standard of value since roughly 3100-2500 BCE, weighing out unstamped chunks of metal by the shekel (originally about 8.4 grams) to price grain, timber, wages, and slaves, establishing the concept of a metallic measure of value long before coins existed.

- The circulation of Hacksilber (cut-up silver pieces) across the ancient Near East showed that pre-coinage societies already transacted in weighed bullion, but the constant need to weigh and assay each lump created a clear practical demand for a pre-certified medium of exchange.

- Lydia possessed an unusual natural resource in the electrum (a roughly 54% gold, 44% silver alloy) panned from the Pactolus River near its capital Sardis, giving the kingdom a ready supply of precious metal to convert into standardized lumps.

- Metalworkers in the region had developed the techniques of casting metal into consistent weights and impressing designs with engraved dies, the technological basis for striking a repeatable stamp onto a metal blank.

- The Lydian monarchy under kings such as Alyattes (reigned c. 619-560 BCE) held enough centralized authority and prestige to guarantee a currency, so that a royal stamp could credibly certify a piece's weight and metal content.

- Sardis sat astride active trade routes between the Greek Aegean cities and the interior of Anatolia, generating a volume of commerce that rewarded any innovation reducing the friction of repeated weighing and testing of metal.

Its Legacy

- The Lydian innovation of stamping electrum lumps with the royal lion's head created the first state-guaranteed money, letting merchants trade by counting trusted, pre-certified pieces rather than weighing and assaying metal for every transaction.

- King Croesus (reigned c. 560-547 BCE) refined the idea by issuing the first coins of nearly pure gold and pure silver, the 'Croeseids,' which gave coins a more definite intrinsic value than ambiguous electrum and made Croesus a byword for wealth.

- Greek city-states rapidly adopted and personalized coinage from around 600 BCE onward, with Athens striking its silver 'owl' tetradrachm (bearing Athena and her owl) in the late 6th century BCE, a coin that became a dominant international trade currency across three continents.

- When Darius I of Persia conquered Lydia he inherited its minting technology and created the gold daric, the first gold coin to circulate widely across an empire, used to pay soldiers, Greek mercenaries, and governmental expenses.

- Coinage enabled standardized state payments to ordinary citizens, such as pay for jury service and assembly attendance in Athens, a development Aristotle identified as characteristically democratic and tied to the shift from aristocratic to civic conceptions of money.

- The principle that an authority's stamp, rather than the metal alone, could guarantee value laid the foundation for later monetary systems, from Rome's denarius to Chinese state-issued paper money under the Song dynasty and ultimately to modern fiat currencies detached from any precious-metal backing.

Myth vs. Reality

Myth: The Lydians invented money, so before coins there was no money — just barter.

Reality: Coins were a late refinement of money, not its origin. Money in the form of weighed silver and grain functioned as a medium of exchange, unit of account, and means of payment in Mesopotamia for roughly two thousand years before the first coins; the silver shekel was used as a standard of value by the mid-third millennium BCE. Anthropologist David Graeber argued in Debt: The First 5,000 Years that credit and accounting preceded both barter and coinage, and that the textbook 'barter economy' that supposedly gave way to money is largely a myth with little ethnographic support. Coins added a state-stamped, standardized, portable form, but money itself was far older.

Myth: The first coins were gold (or silver) coins, like the famous coins of King Croesus.

Reality: The earliest Lydian coins were struck from electrum, a naturally occurring pale alloy of gold and silver (often further adjusted with added silver and copper). Herodotus wrote that the Lydians were the first to strike coinage of gold and silver, but the earliest issues actually predate pure-metal coins. Genuine bimetallic gold-and-silver coinage was a later innovation credited to Croesus (reigned mid-6th century BCE), well after the first electrum coins appeared under earlier Mermnad kings such as Alyattes.

Myth: Coinage was a single invention in Lydia that then spread to the rest of the world.

Reality: Coinage arose independently in at least three regions. Lydia in western Anatolia produced the first electrum coins in the late 7th century BCE, but China developed its own cast bronze coinage (spade and knife money, then round coins) on a separate trajectory, possibly as early as the Lydian coins, and India developed punch-marked silver coins. China's tradition in particular is widely held to have emerged independently of the Western, Lydian-derived line that influenced Greek, Persian, and later coinages.

Myth: The first coins were everyday small change, invented to make shopping in the marketplace easier.

Reality: The earliest electrum coins were strikingly high in value, not pocket money. Scholars estimate that the common third-stater (trite) was worth on the order of a month's subsistence, and even the smallest fractions (down to 1/96 stater) were roughly a day's wage. Such denominations were poorly suited to buying a loaf of bread. This has led numismatists and historians to argue that early coinage served large-scale state purposes — paying soldiers and mercenaries, fines, taxes, and dues — and that the convenience of coins for ordinary retail trade was a consequence that developed later rather than the original motive.

Myth: We know the precise year coinage was invented.

Reality: There is no firm date. Scholarly estimates for the earliest Lydian coins range across the 7th into the 6th century BCE, commonly placed in the second half of the 7th century. A key anchor is a deposit of early coins found beneath the Temple of Artemis at Ephesus, but the dating of that deposit is itself debated, and chronologies that depend on Herodotus's regnal dates for Lydian kings have been challenged and revised by numismatists. Confident-sounding specific dates such as 'around 630 BCE' or '600 BCE' are best read as scholarly estimates within a contested range, not established fact.

In Their Words

"they were the first of men, so far as we know, who struck and used coin of gold or silver; and also they were the first retail-traders." — Herodotus, Histories 1.94.1 (on the Lydians), trans. G. C. Macaulay

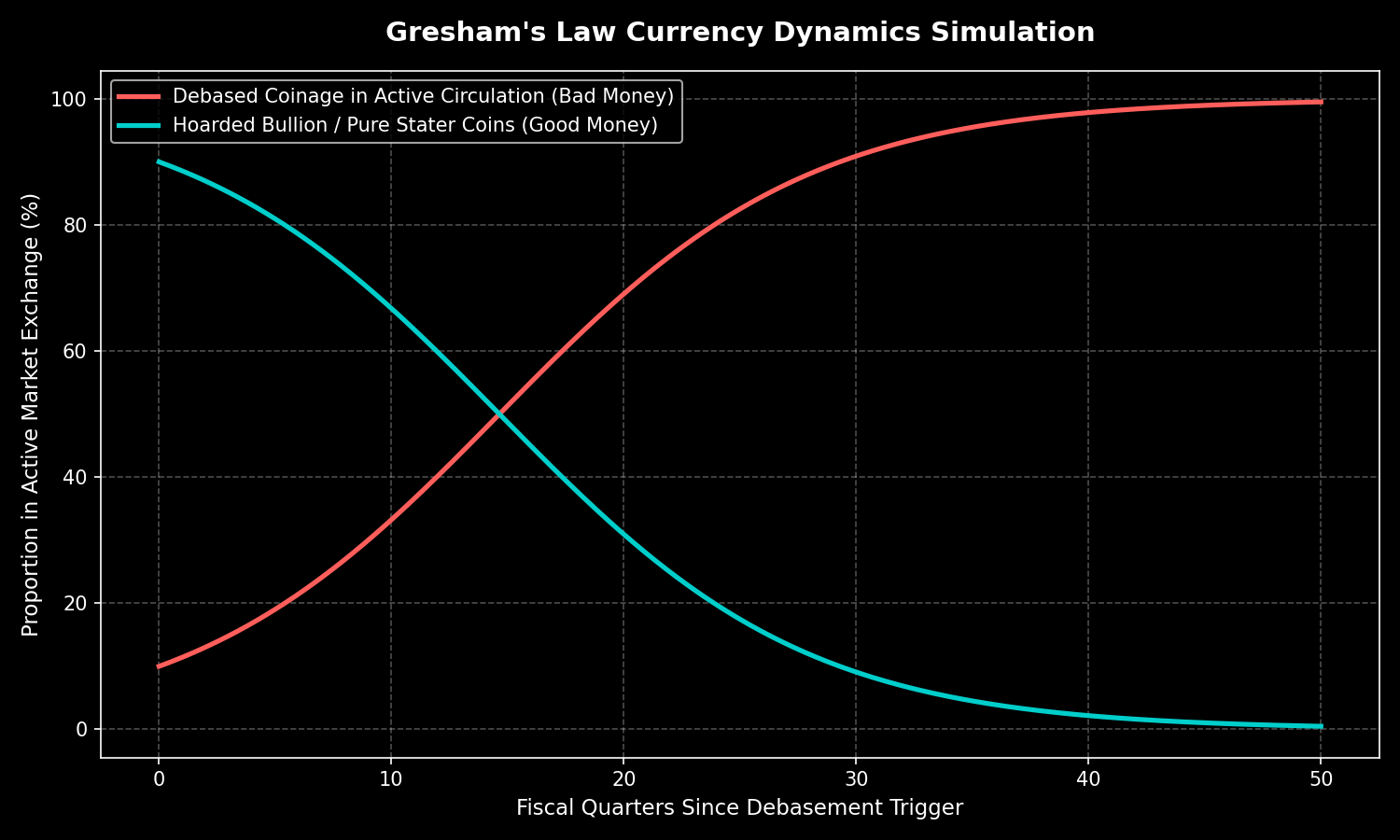

Data Visualization

References & Sources

- History of coins — Wikipedia

- David M. Schaps, The Invention of Coinage and the Monetization of Ancient Greece (University of Michigan Press, 2004)

- Richard Seaford, Money and the Early Greek Mind: Homer, Philosophy, Tragedy (Cambridge University Press, 2004)

- Robert W. Wallace, 'The Origin of Electrum Coinage,' American Journal of Archaeology 91.3 (1987)

- Koray Konuk, 'Asia Minor to the Ionian Revolt,' in The Oxford Handbook of Greek and Roman Coinage (ed. W. E. Metcalf, 2012)

- John H. Kroll, 'The Coins of Sardis,' in Sardis: A Roman and Modern Lydian City (Archaeological Exploration of Sardis)